Good morning top dog traders of the Evil Speculator domain of the internet. I’m sipping my bullet proof decaf cafe’ this morning after I spent some time putting together my tunes for my DJ set at Afrika Burn this year. AfrikaBurn, South Africa’s sanctioned version of Burning Man, takes place about 6 hours outside of Cape Town in the middle of the African desert in late April. It’ll be my first experience living from a make shift home in a Backie which is the South African equivalent of a U-Haul.

The idea is a break from EDM that’s available elsewhere on the playa 24/7, starting off with the Crying In Coffee Houses set from one of my campmates. For my set, with the theme of keeping with a break from the EDM, I’ll be doing the The New Orleans Jazz Parlor. Featuring the lovely ladies of the Shake’Em Up Jazz Band I discovered on a trip to New Orleans at the infamous Spotted Cat last month. If New Orleans jazz is your thang, these ladies bring it with unique flavor.

Speaking of flavor, if you’ve followed along any of my previous posts, you probably know by now that my style of trading is not sitting in front of the computer all day looking at charts. Some of my beliefs about trading:

- My mood and my mental states effect my trading, even if I don’t think they do.

- That as a human, I’m never subjective, even though I think I am. My subconscious beliefs are running the show.

- That when it comes to trading, it’s a statistics game.

- Computers are better at statistics than I am.

- Sitting in front of the computer all day, staring at charts, sucks. I have better things to do.

- Computers are better than I am at staring at charts all day and making by-the-numbers analysis.

- Bar charts are not the best way to make decisions about trading, they are just one way of looking at information.

In the year 2020, powerful and easy-to-do backtesting platforms are everywhere. I’d say with little exception that just about any subjective and discretionary trader could back test their trading. And the reason they choose not to? Because they know they’ve been running on luck and what they are doing has little or no edge.

As such, my trading is by the numbers baby. More specifically, statistics. When it comes to the overall market, the most important metric in my trading is the…

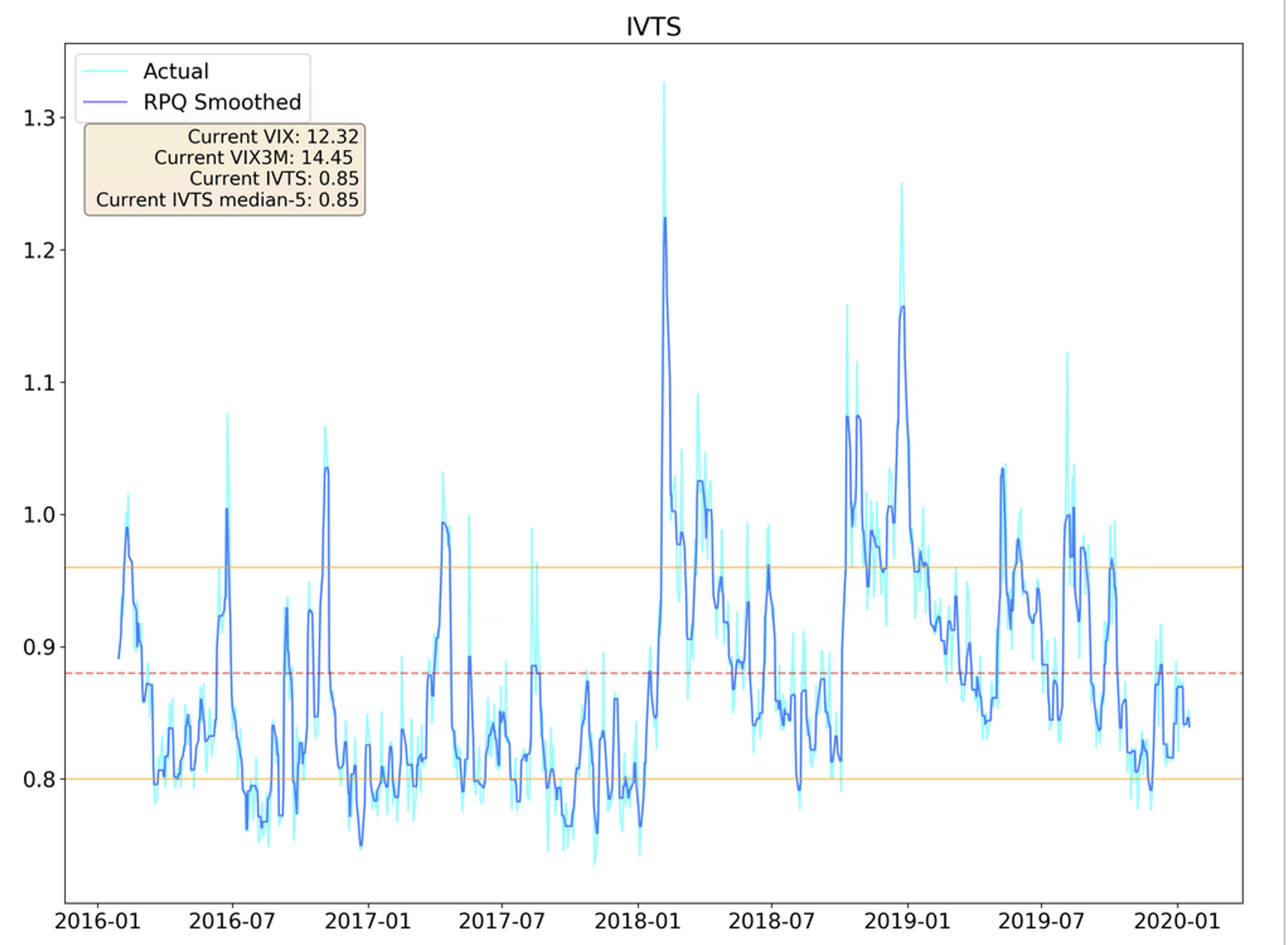

The IVTS, or the implied volatility term structure is simply my go-to. It determines which market regime I’m dealing with and which one I’m likely to see on the horizon at some point. The formula for the IVTS is:

It’s the VIX over the VIX3M, both readily available from Yahoo Finance as symbols ^VIX an ^VXV. The VIX3M was formally known as VXV before the CBOE changed it a few years back. It’s pretty simple and as I write this, the VIX is 12.72 and the VIX3M is 14.87, pegging the IVTS at .86.

WHY THE IVTS MATTERS

As a regular trader, you’re probably not up on the geeky quant papers published in the professional trading world. If you look at the tons of papers published by PhD quant dorks, there are literally 100s of papers published on the IVTS or it’s derivatives. It’s probably one of the most researched areas of quant finance. Why is this?

The reason is quite simple. Most indicators tell us about the past. The VIX3M tells us what the market believes about volatility 3 months out. Not now, in 3 months. By it’s nature, the VIX3M tells us about the future.

The VIX tells us what’s essentially happening right now, in the short term. And when we put the VIX and VIX3M together, it’s pure magic because it also takes into account another magical property of the IVTS: it’s mean reverting.

The mean IVTS value for the past 10 years is .88 with a standard deviation of +/- .08. The mean is the red dashed line at .88 and the orange lines are +/- .08. If you do geek mean reversion tests on the IVTS, it scores as highly mean reverting. More so than just about any other financial instrument.

HOW TO USE IT

OK, we get it, it’s mean reverting and tells us what the market thinks about future volatility.. which really tells us what the market thinks about the direction for the market in 90 days. Why the IVTS is so heavily researched is because it’s used to make trading decisions from. It tells us what types of markets we’re dealing and what types of trades have a much higher statistical probability of success, based on the IVTS.

When we are in slow marching bull markets, values tend to be below the mean of .88. And when we’re in viscous sell offs, it tends to spike over 1.0. We can see during the volatility melt down in February 2018, it spiked to 1.3. Many quant funds use the IVTS to get in and GTFO of long equity exposure (or shift it around in some way). Whales move markets and we want to ride on their coat tails.

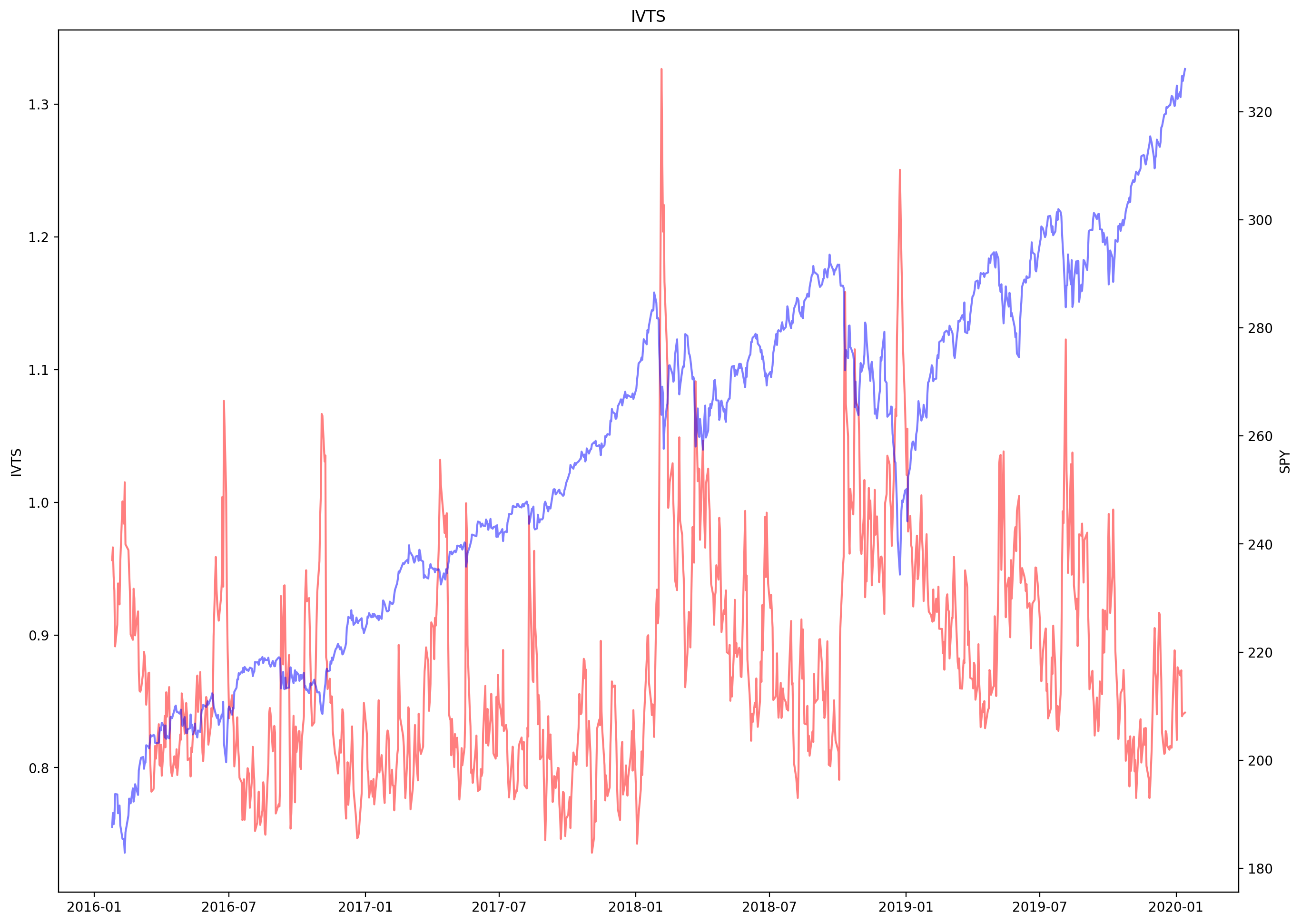

The red line above is the IVTS, the blue SPY. It’s not exactly a revelation that when SPY is selling off hard like in early 2018, that IVTS is spiking hard. The IVTS is about as close as we will ever get to the canary in the coal mine for long market exposure.

However we’re not whales and much more nimble than a $5 billion dollar fund. This allows us to take greater advantage of the IVTS than even the super smart people who’ve researched it to death (thank you guys!). The IVTS allows us to extend our edge in trading substantially.

And now for the subs, we’re going to take a lovely trade from the IVTS playbook for this week that has stacked up piles of R bricks for me since early fall 2019.

Please log in to your RPQ membership in order to view the rest of this post. Not a member yet? Click here to learn more about how Red Pill Quants can help you advance your trading to the next level.